As more and more people have taken an interest in monetary affairs — especially in the Fed and its various operations — in recent years, many people have joined the discussions related to these matters, especially on the World Wide Web. In reading these posts over the years, in particular in reading the comments on a post I placed recently at The Beacon, I have been struck by the frequency with which the writers reveal that they do not understand a basic conceptual matter in regard to money, monetary policy, and the Fed. That matter is the difference between the monetary base and the money stock.

In the data compiled by the Fed and used by analysts in various ways, the monetary base (sometimes called “high-powered money” or “base money”) consists of currency — that is, Federal Reserve notes, the legally authorized, circulating paper money denominated in U.S. dollars issued by one of the Federal Reserve System’s regional banks — plus deposits that commercial banks and other “depository institutions” hold as reserves in accounts at the Fed. This sum is known as the monetary base because it forms the foundation on which commercial banks may extend loans to customers and make investments by means of establishing checking accounts (checkable deposit accounts) for those customers or security sellers.

In a fractional-reserve banking system, such as that in the United States and most other countries, banks are legally required to hold a certain percentage of their deposit liabilities (including those they create as just described) as reserves at the Fed. If they hold more reserves with the Fed than their current accounts require, those reserves as denominated “excess reserves.” These may be used, of course, to extend additional loans and make additional investments in securities until the bank has reached a condition in which it has used up all of its legally “excess” reserves.

As a fractional-reserve banking system creates new checking accounts for its customers, it adds to the money stock, which is the set of all highly liquid assets that are most readily exchangeable for goods and services. Note, however, that the precise definition of the money stock is necessarily vague: exactly which liquid assets ought to be counted as “money” and which ones ought not to be counted cannot be resolved by finding the “correct” answer; there is no correct answer. What one would wish to count depends on the question one seeks to answer by making reference to the amount of “money” in the system.

Therefore, one finds that many different statistical series are created and employed by economists and financial analysts. These are denominated by acronyms such as M1, M2, M3, MZM, and so forth. There is no conspiracy or attempt to conceal anything in this way of dealing with the data, but only a frank recognition that “money” is not a clearcut economic entity, and indeed its composition may change — and often has changed in the past – as economic and financial conditions and transaction practices vary.

It is common to say that the Fed and other central banks have the power to “create money out of thin air,” that is, out of nothing more than their own declaration that new deposits are now available to a bank at the Fed (often in exchange for a bank’s asset or collateral). This common saying, however, is not quite right. In fact, the Fed has only the power to create new base money. If the banks that acquire that new base money in their accounts do not use it to make new loans or purchase new investment securities, it simply sits there at the Fed: in that form, it is not money because it is not a balance that can be exchanged directly for goods and services. For the Fed to create money, then, it must have the cooperation of the banks, which use the newly created base money to establish new checking accounts for loan customers or security sellers.

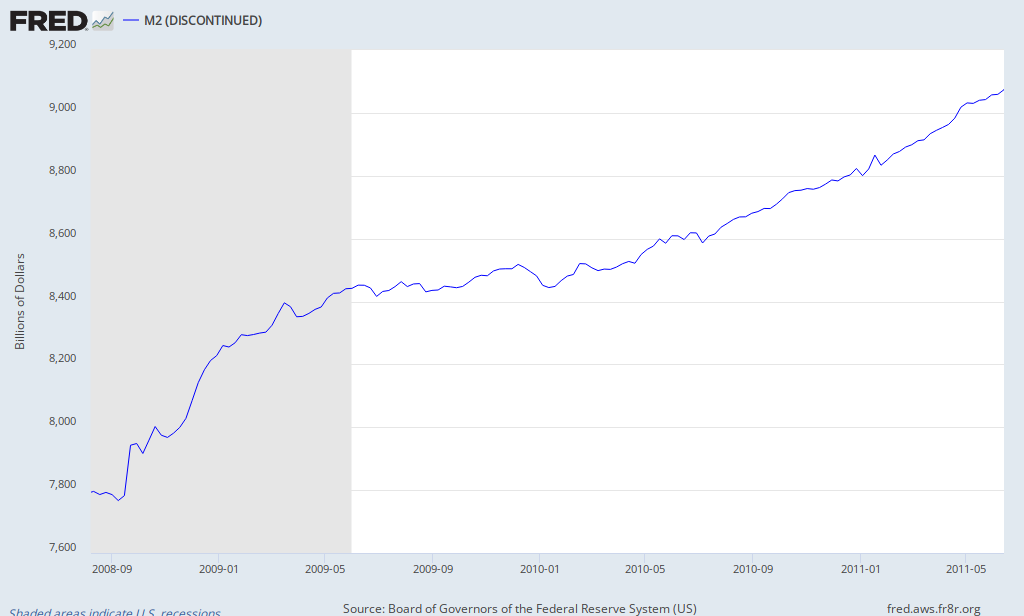

This is the situation to which my previous post called attention: namely, that since August 2008, the Fed has created a fantastically huge addition to the monetary base, about $1.5 trillion dollars, yet the banks have let the lion’s share of this addition lending potential sit at the Fed unused, hence untransformed into increases in the money stock.

For example, M2, a commonly used measure of the money stock, has increased by only about $1.244 billion, or about 16 percent since August 2008. Whereas the “money multiplier” associated with additional base money might normally have been expected to be perhaps 10 or more, turning $1.5 trillion of new base money into $15 trillion of newly created money stock (and thereby triggering hyperinflation), in the present case, the addition to the money stock has actually been smaller than the addition to the monetary base — that is, the money multiplier has been less than one because of the banks’ not making use of the new lending potential it gives them.

This difference — this breakage, as it were, of the previously prevailing relation between the monetary base (which the Fed controls) and the money stock (which the Fed and the banking system and its customers jointly control) — is the essence of the puzzle to which I called attention in my previous post. Many people have offered plausible explanations for it, but many of the lay commentators’ comments are flawed by a failure to appreciate correctly the distinction between the monetary base and the money stock. Intelligent engagement in this discussion requires that one master this elementary yet critical distinction.