Meanwhile, during the same period, the excess reserves that commercial banks hold at the Fed have increased from $2 billion in August 2008 to $1.513 billion in May 2011.

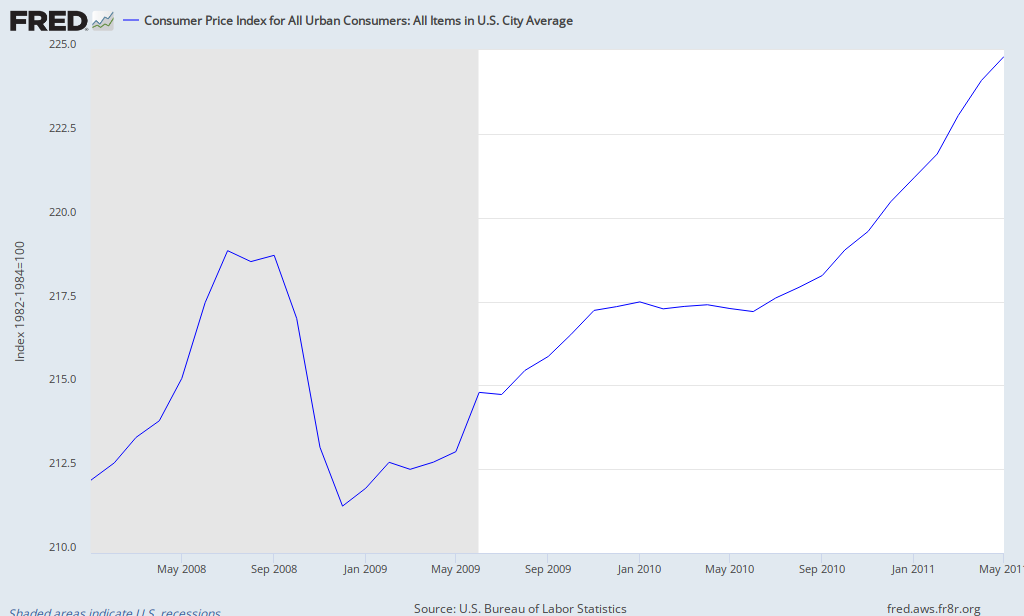

Ordinarily, one would have expected this development to produce hyperinflation of the general price level. However, the price level has increased quite moderately, and for a while many analysts warned that deflation was the greater risk. Despite a slight increase in the price level’s rate of growth in recent months, the index of prices paid by all urban consumers has increased by only about 6 percent in the three and a half years since the beginning of 2008. Not only has hyperinflation failed to appear; even garden variety inflation of prices in general has been extremely low by the standard of recent decades.

The preceding combination of events poses a great challenge to economic analysts. How can we explain that the fantastically enormous explosion of bank reserves has not given rise to bank lending that would greatly expand the money stock and thereby drive up prices in general?

The most obvious answer, of course, is that the banks are simply sitting on the reserves, rather than lending them to customers. And why are they doing so? The usual answer is that since late 2008, the Fed has paid the banks a rate of interest on their reserves at the Fed. This interest rate has recently been in the range 0-0.25 percent. Although this is not nothing, it verges very closely on nothing. And if one notes that the purchasing power of money has fallen at least a bit, it is clear that the banks are realizing a negative real rate of return on their holdings of excess reserves at the Fed.

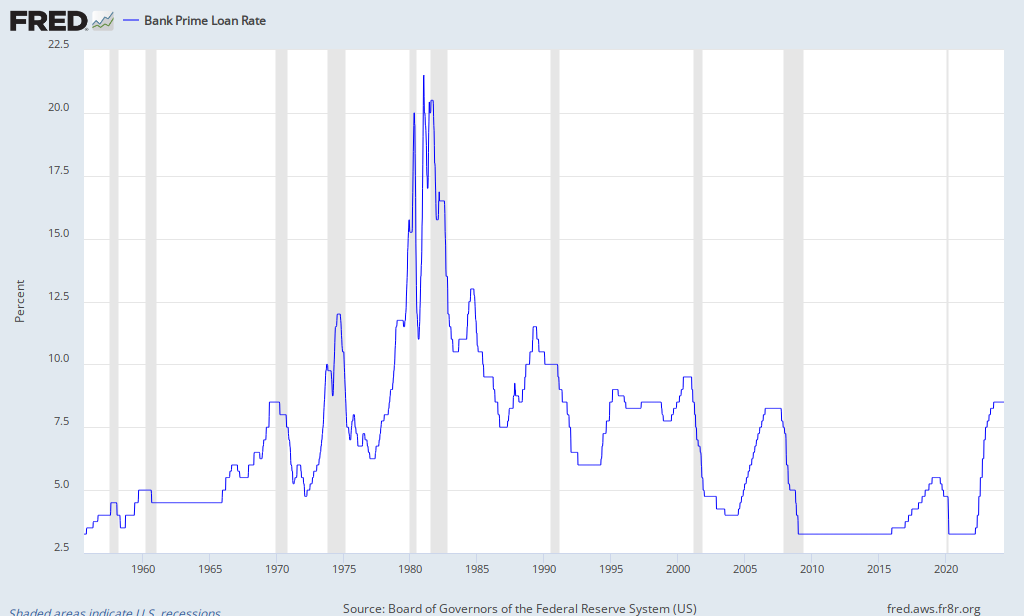

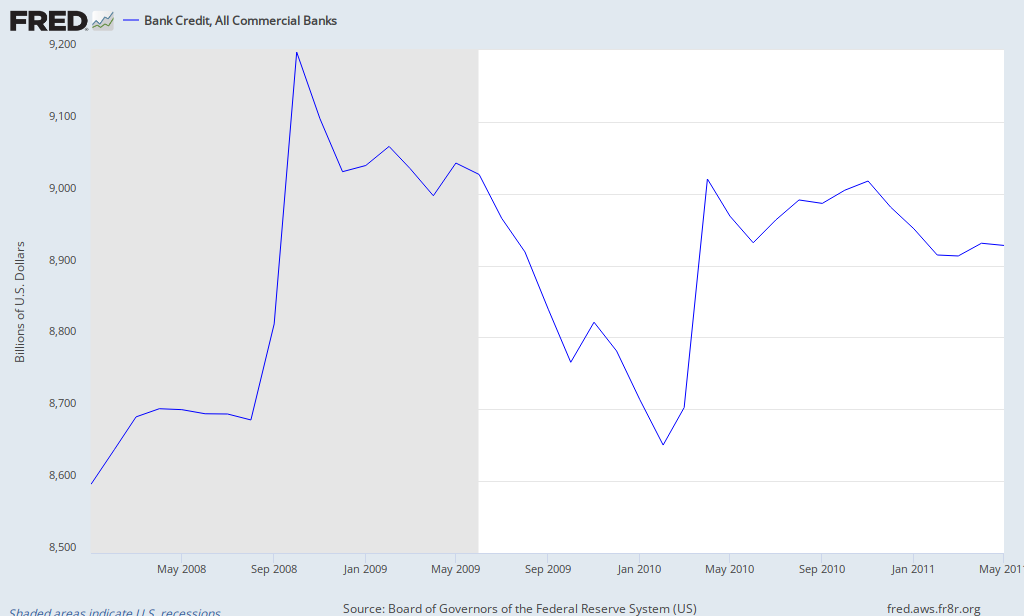

Moreover, they are doing so notwithstanding that they appear to have the option of lending at 3.25 percent to their best corporate customers and at higher rates to their less creditworthy customers. Why are they foregoing the opportunity to earn huge sums by switching out of excess reserves at the Fed into commercial loans and investments? The answer would seem to be that that are so frightened of the risk associated even with loans to their best customers that they are loath to lend. After some volatility up and down and then up again between the summer of 2008 and early 2010, total loans and investments of all commercial banks have settled for more than a year at a level only about 2 percent greater than their level at the beginning of 2008. This increase of about $200 billion amounts to only a small fraction, about 13 percent, of the increase in their excess-reserve balance at the Fed during the same period.

In these circumstances, some economists have taken to arguing that excess reserves no long constitute “high-powered money,” that they no longer belong to the monetary base, and therefore they have not proved to be the fuel for hyperinflation that nearly all economists would have expected them to be prior to the past four years of anomalous experience.

I am not convinced. First, I am not convinced that these gigantic sums will not, sooner or later, still become the fuel for hyperinflation, or at least for a greatly accelerating rate of general price inflation, which economists expected they would be before the recent recession and all of the government’s and the Fed’s extraordinary responses to it occurred. Second, I am not convinced that the banks will remain content forever with earning a negative real rate of return on their holdings of $1.5 trillion in excess reserves now languishing at the Fed. If they were to realize only the difference between the rate the Fed is paying them and the rate they would earn by lending these funds exclusively to prime customers — an increase of 3 percent on their return — they would gain an additional $45 billion in income. That’s a great deal of potential income to leave lying on the table, and it might be even greater if we factored in the additional income they might earn by lending to less-than-prime customers at greater rates. I understand, of course, that banks are seeking to repair their damaged balance sheets, in light of their recent debacle in real-estate-related investments of various sorts and in conformity with the new Basel requirements for increased bank capitalization. Still, I am not convinced that these consideration can account fully for the very curious conditions now existing in the banking industry.

Of course, my lack of conviction in the new wisdom may be groundless. This time, everything really may be different. But as an economic historian, as well as an economist well behind the cutting edge of his profession, I am not ready to latch onto this latest “this time it’s different” explanation, at least not until a long time has passed and my skepticism has been proved baseless by long-sustained counter experience. At the moment, the conjunction of recent macroeconomic events still seems to me to pose a great puzzle.

Perhaps a part of the answer relates to the regime uncertainty about which I have written from time to time during the past three years, harkening back to my earlier writing about its significance during the second half of the 1930s, during the so-called Second New Deal. It would hardly be astonishing if such worries were now contributing to the extreme risk aversion banks are manifesting. Moreover, perhaps for the same reason, potential borrowers are not exactly clamoring for loans, and indeed many corporations are sitting on huge cash hoards of their own. Interesting times, indeed.